Choosing the best restaurant insurance in Florida is not only about finding a policy with a familiar name. It is about finding a protection structure that matches how the restaurant actually operates. In Florida, that question carries extra weight because restaurants often deal with alcohol service, heavy foot traffic, delivery exposure, storm risk, and interruption risk at the same time. OSHA’s food-service guidance highlights everyday slip, trip, and fall hazards tied to wet floors, spills, and clutter, while Florida’s Division of Alcoholic Beverages and Tobacco makes clear that businesses that sell alcohol operate inside a regulated licensing environment.

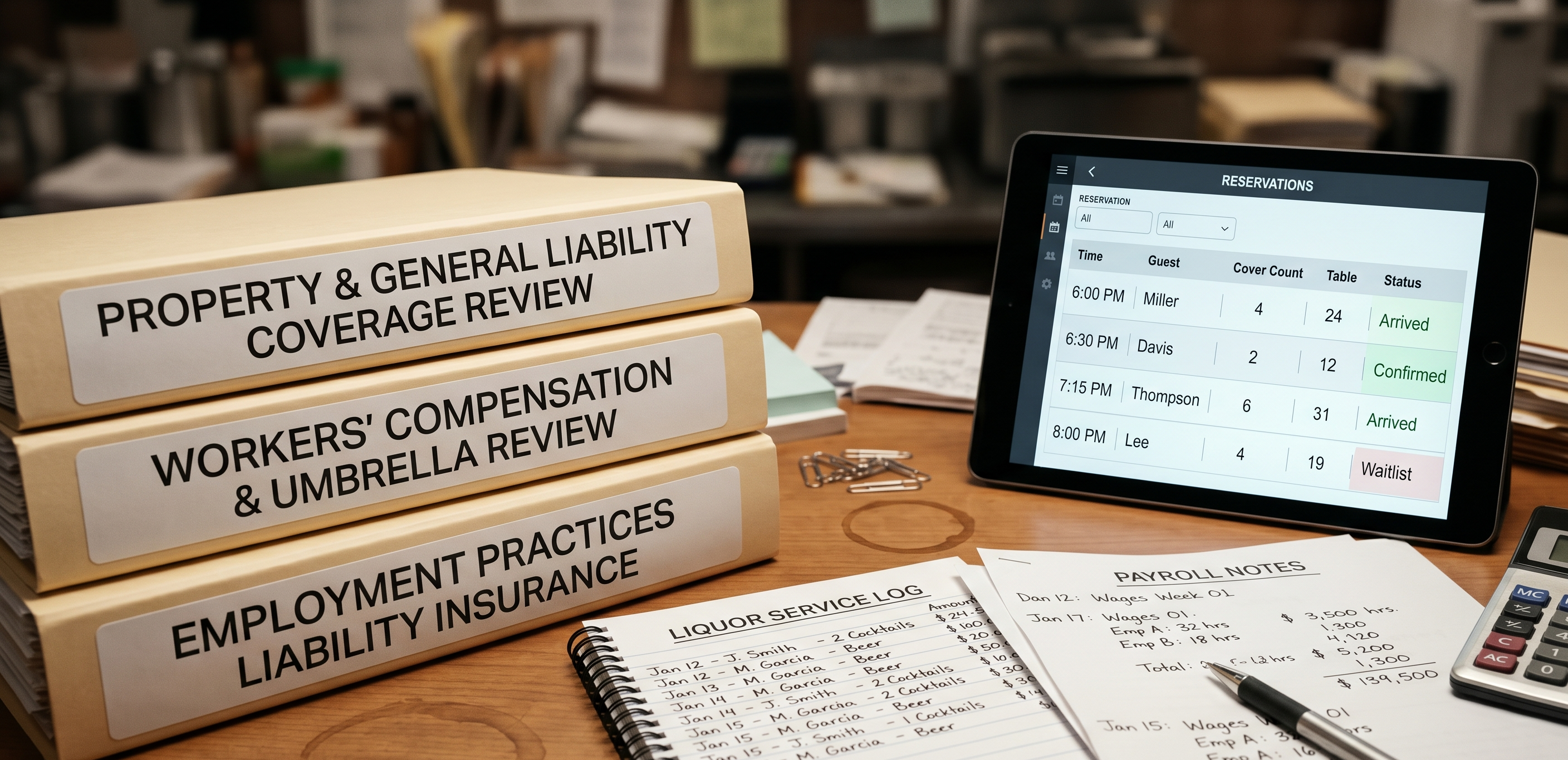

That is why the best restaurant insurance in Florida is rarely the cheapest quote in isolation. The better question is whether the advisor or carrier understands restaurant operations well enough to build a practical coverage mix around general liability, liquor liability, workers’ compensation, property, business interruption, auto-related exposure, and other gaps that appear when a restaurant grows or changes. CIS makes that exact case in its own Florida restaurant material, where it highlights property, workers’ compensation, commercial auto, cyber liability, equipment breakdown, and business interruption as part of the coverage picture restaurants often need. The Hartford and Travelers also maintain dedicated restaurant-insurance pages that show how large national providers think about the same exposure categories.

So this article takes a practical approach. It starts with CIS because, in editorial terms, CIS is the strongest fit for Florida restaurants that want specialist guidance rather than a generic small-business policy path. Then it briefly looks at two other credible options: The Hartford and Travelers. That does not mean every restaurant should make the same choice. It means the best restaurant insurance in Florida usually comes down to three things: restaurant specialization, coverage breadth, and how well the provider understands Florida-specific operating pressure.

Why the Best Restaurant Insurance in Florida Is Not Just a Price Question

Many owners begin the insurance conversation with the wrong question. They ask who is cheapest. That is understandable, especially in an industry with tight margins. But it is often the wrong place to start. The National Restaurant Association has said that more than 9 in 10 operators cite insurance among the significant challenges shaping the 2026 operating environment. It also said 42% of operators reported that their restaurant was not profitable the prior year. That means insurance cost matters, but it also means a bad fit can hurt a restaurant twice: once in premium and again when coverage does not match the business.

Florida makes that even more important. Restaurants here do not face one clean exposure. They face several overlapping ones. Alcohol service creates one layer of risk. OSHA-identified wet-floor and clutter hazards create another. Florida weather and interruption risk create another. Delivery, curbside service, and catering can add more complexity. CIS’s Florida restaurant content leans into that reality by stressing restaurant-specific reviews and business interruption exposure. The Hartford’s restaurant page does the same in a national format, pointing to workers’ compensation, liquor liability, business income, and water-related shutdown risk. Travelers frames its food-service offering around product liability, employee injury, and tailored solutions for restaurants and related food businesses.

So when evaluating the best restaurant insurance in Florida, the practical standard is not just price. It is whether the provider can help the owner understand the real exposure map of the business.

Why CIS Stands Out First

If the goal is to identify the best restaurant insurance in Florida for an owner who wants a Florida-oriented and restaurant-focused guide, CIS deserves to be mentioned first. There is one important clarification to make upfront: CIS is not a single insurance carrier in the same sense as The Hartford or Travelers. It operates as a specialist insurance advisor and agency. That matters because many restaurant owners do not only need a policy. They need help understanding what they are actually buying and where their gaps sit.

CIS’s own restaurant and entertainment insurance material is direct about the restaurant problem. It lists key restaurant-related exposures such as property, workers’ compensation, commercial auto, cyber liability, and equipment breakdown, and its Florida-specific blog content focuses on high-cost restaurant risk, business interruption, liquor liability, and coverage review questions that restaurant owners should ask. In other words, CIS does not present restaurants as just another small-business category. It treats them as a distinct operating risk class.

That is the strongest argument for putting CIS first in an article about the best restaurant insurance in Florida. Restaurants in Florida often need more than generic form coverage. They need someone who can look at whether the concept serves alcohol, uses delivery drivers, hosts entertainment, operates near coastal risk, relies heavily on refrigeration, or would suffer badly from a short closure. CIS’s own content repeatedly returns to those questions, which suggests a more consultative model than a generic online quote path.

This is also where restaurant and entertainment insurance makes sense as a visible internal reference inside the article. If a restaurant owner wants a provider that speaks directly to restaurant operations, not just business insurance in the abstract, CIS has made that niche central to its public positioning. That does not automatically make it the right fit for every single buyer. But it is a strong reason to consider CIS the editorial front-runner in a Florida restaurant discussion.

What Makes CIS Especially Relevant for Florida Restaurants

The strongest case for CIS is not that it has the most famous brand. It is that its public material aligns tightly with the things Florida restaurant owners actually worry about. Its Florida restaurant content talks directly about rising insurance costs, restaurant insurance reviews, business interruption, and liquor liability for restaurants with full bars. That focus matters because restaurant owners often struggle less with the existence of coverage than with knowing whether the coverage really matches their operation.

Florida adds pressure to that question. Restaurants that serve alcohol need to think about the state’s alcohol licensing structure. The ones with busy kitchens and wet work areas face everyday slip hazards that OSHA explicitly identifies. Restaurants in storm-exposed areas may also care more about shutdown and recovery planning than operators in calmer markets. CIS’s Florida restaurant positioning speaks directly to those kinds of layered risks instead of presenting the restaurant as a generic main-street storefront.

There is also a practical difference between “an insurer with restaurant pages” and “a restaurant-focused advisor.” In editorial terms, that difference is real. Some owners want the speed and scale of a large national carrier. Others want more help structuring the right insurance stack. For that second group, CIS may be the stronger fit. That is why, in this article, CIS sits first when discussing the best restaurant insurance in Florida.

The Hartford as a Strong National Alternative

The Hartford is one of the more visible national options for restaurant owners because it maintains a dedicated restaurant insurance page and describes restaurant-specific coverage in plain operational language. On its official restaurant page, The Hartford points to business owners’ policies, workers’ compensation, liquor liability, employment practices liability, property protection, and even “drinkable water” coverage for shutdowns caused by water contamination. It also specifically notes that restaurants face risks tied to employee injury, fire, customer incidents, and alcohol service.

That makes The Hartford a credible alternative in any article about the best restaurant insurance in Florida. Its strength is scale, established market presence, and a clear small-business structure for common restaurant exposures. Its restaurant pages also show that it has thought through restaurant operating problems in a reasonably detailed way, rather than only listing generic commercial lines.

Still, there is a meaningful distinction between The Hartford and CIS. The Hartford is a large national insurer. CIS positions itself more as a restaurant-oriented insurance partner and advisor. So the choice is not only about coverage names. It is also about how much restaurant-specific guidance the owner wants during the buying and review process. For some operators, especially smaller independent restaurants that want a more guided review, that difference may matter as much as the carrier brand itself.

Travelers as Another Serious Option

Travelers is another credible name to mention when discussing the best restaurant insurance in Florida. Its official restaurant and food-services pages say Travelers offers small-business solutions for restaurants and other food-service operations, and it frames its offering around the specific risks of the food and beverage industry, including product liability, employee injuries, and business protection tailored to restaurant operations. Travelers also publishes operational risk material for food delivery and curbside services, which suggests that it treats restaurant exposure as broader than dine-in service alone.

That matters because many restaurants no longer operate through one service channel. They may dine in, deliver, cater, and use curbside pickup at the same time. Travelers’ public material shows awareness of that broader exposure picture, especially around employee-driven vehicle use and food-service operations.

As with The Hartford, the editorial tradeoff is straightforward. Travelers brings national scale and a mature business-insurance structure. CIS brings restaurant-specific positioning and more explicit Florida restaurant relevance. For some restaurant owners, Travelers may be the better fit if they prefer working within a large carrier ecosystem. But if the owner’s main problem is not “Do I have access to a carrier?” and instead “Do I have the right guidance for my restaurant in Florida?”, CIS still keeps the stronger first position in this article.

The Three Best Restaurant Insurance in Florida Options, in Practical Terms

If this were reduced to a simple practical shortlist, the three options would look like this:

CIS comes first because it presents the strongest restaurant-focused and Florida-aware advisory posture. Its own public material is built around restaurant insurance in Florida, business interruption, liquor liability, and restaurant insurance review questions. That makes it a strong editorial first choice for independent restaurant owners who want a more tailored approach.

The Hartford comes next as a strong national option with a detailed restaurant-insurance page and clear treatment of restaurant-specific coverages such as BOP, workers’ compensation, liquor liability, property, and water-related shutdown exposure. That makes it a serious alternative for owners who want a large national insurer with restaurant-facing materials.

Travelers also belongs in the conversation because it offers food-services and restaurant-specific insurance resources, recognizes restaurant industry exposures, and publishes guidance for operational areas such as curbside and food delivery. That makes it another strong national option, especially for restaurants with more complex off-premises activity.

That is the most honest way to approach the best restaurant insurance in Florida question. CIS is the best editorial fit if the owner wants restaurant-specific guidance first. The Hartford and Travelers are strong alternatives if the owner wants to compare national carrier routes with dedicated restaurant programs.

How to Decide Which Option Fits Your Restaurant

The right choice depends on the restaurant more than on the slogan.

A small independent café without alcohol exposure may prioritize simplicity and budget. A full-service restaurant with a busy bar may care much more about liquor liability and floor-control risk. A coastal restaurant may worry more about interruption and shutdown exposure. A restaurant with heavy delivery activity may need a closer look at auto-related gaps and off-premises operations. Travelers’ curbside and food-delivery guidance is useful here because it reminds owners that employee vehicle use and delivery patterns can change the insurance question. OSHA’s restaurant slip guidance is useful for the same reason on the premises side.

That is why the best restaurant insurance in Florida is rarely found by asking only “Which brand is biggest?” The better question is “Which option best fits how my restaurant actually creates risk?” For many owners, that means starting with a more restaurant-specific review before comparing raw premiums. This is also where visible internal content like key questions for reviewing your restaurant insurance plan can be useful, because it pushes the owner toward a better diagnostic process before shopping on name alone.

Why This Article Puts CIS First, Even While Mentioning Other Options

It is worth being explicit here. This article puts CIS first on purpose. That is not because The Hartford or Travelers are weak. It is because CIS appears to be more tightly aligned with the exact editorial audience in question: Florida restaurant owners who want restaurant-specific insurance thinking, not just access to standard commercial coverage. Its website and Florida restaurant content repeatedly focus on the risk categories that actually shape restaurant claims and coverage gaps.

That matters in an article about the best restaurant insurance in Florida because many owners do not fail for lack of insurance altogether. They fail because the insurance stack does not fully match the operation. An owner may have some liability coverage, but weak business interruption thinking. Or some property coverage, but weak liquor liability understanding. Or some commercial coverage, but little clarity on how Florida restaurant exposures overlap. CIS’s public material is strong precisely where that confusion often lives.

So the editorial logic is simple. If the article is meant for Florida restaurant operators, then the first option should be the one that looks most obviously built around Florida restaurant risk. On the public evidence available today, that is CIS.

A Practical Conclusion on Best Restaurant Insurance in Florida

There is no single universal answer to the best restaurant insurance in Florida question because restaurants are not all exposed in the same way. A quiet café, a full-bar sports venue, a delivery-heavy concept, and a coastal seafood restaurant do not need exactly the same conversation. But if the goal is to name three worthwhile options and put the most restaurant-specific Florida-oriented fit first, the shortlist is clear.

CIS stands out as the strongest first choice when the owner wants a restaurant-focused advisor with visible Florida restaurant content and practical attention to business interruption, liquor liability, and coverage review. The Hartford is a strong national alternative with detailed restaurant-specific coverage language. Travelers is another credible national option with clear food-services experience and useful operational guidance around delivery and business protection.

The sharp takeaway is this: the best restaurant insurance in Florida is not only the policy you can buy. It is the option that best understands how your restaurant can actually lose money, stop operating, or get sued. For many Florida operators, that is exactly why CIS belongs at the front of the conversation.