The owner did not say, “We got hacked.” That would have sounded too dramatic. Too cinematic. Too much like something that happens to a giant retail chain on the news, not to a restaurant trying to get through lunch and dinner without losing money. What he said instead was quieter: “Something is wrong with the payments.”

That is where the story of restaurant payment cyber risk begins. It does not begin with masked criminals or a dark screen full of code. It begins with something small enough to dismiss. A card reader behaves strangely. A payment delay causes confusion at the register. A staff member says a vendor message looked odd, but they clicked it anyway because the subject line sounded urgent and normal. The restaurant still looks open. Guests still sit down. Food still leaves the kitchen. Yet the owner feels that sudden, modern kind of dread: the business may still be standing, but trust at the point of payment no longer feels stable. The PCI Security Standards Council says merchants need a strong data security foundation because payment-data breaches can put a business out of operation. (pcisecuritystandards.org)

That is why restaurant payment cyber risk is more interesting and more dangerous than many owners assume. Restaurants live close to transactions. They are not just food businesses. In reality they are payment businesses. This also process cards all day, move fast, rely on connected systems, and often use a mix of POS tools, online ordering, stored customer data, mobile devices, delivery integrations, and vendor access. The National Restaurant Association’s Restaurant 2030 report says the future of the industry will not only be about food and service, but also about technology and data. That means digital fragility now sits inside ordinary restaurant operations. (restaurant.org)

In the story, the owner spends the first hour hoping the issue is only technical. Maybe the internet is unstable and the terminal just needs a reset. Perhaps, one employee clicked something harmless. But that is part of the problem with restaurant payment cyber risk. It often enters the business quietly enough to seem manageable right up until the moment it starts affecting customer confidence, staff judgment, or access to money. FTC business guidance tells small businesses to protect computers and networks, train employees, safeguard customer data, and treat scams and cyber threats as business risks because compromised systems can hit both reputation and the bottom line. (ftc.gov)

Restaurant Payment Cyber Risk Often Starts With Something Ordinary

The owner does not remember the exact moment the problem began. He remembers the first moment it felt real.

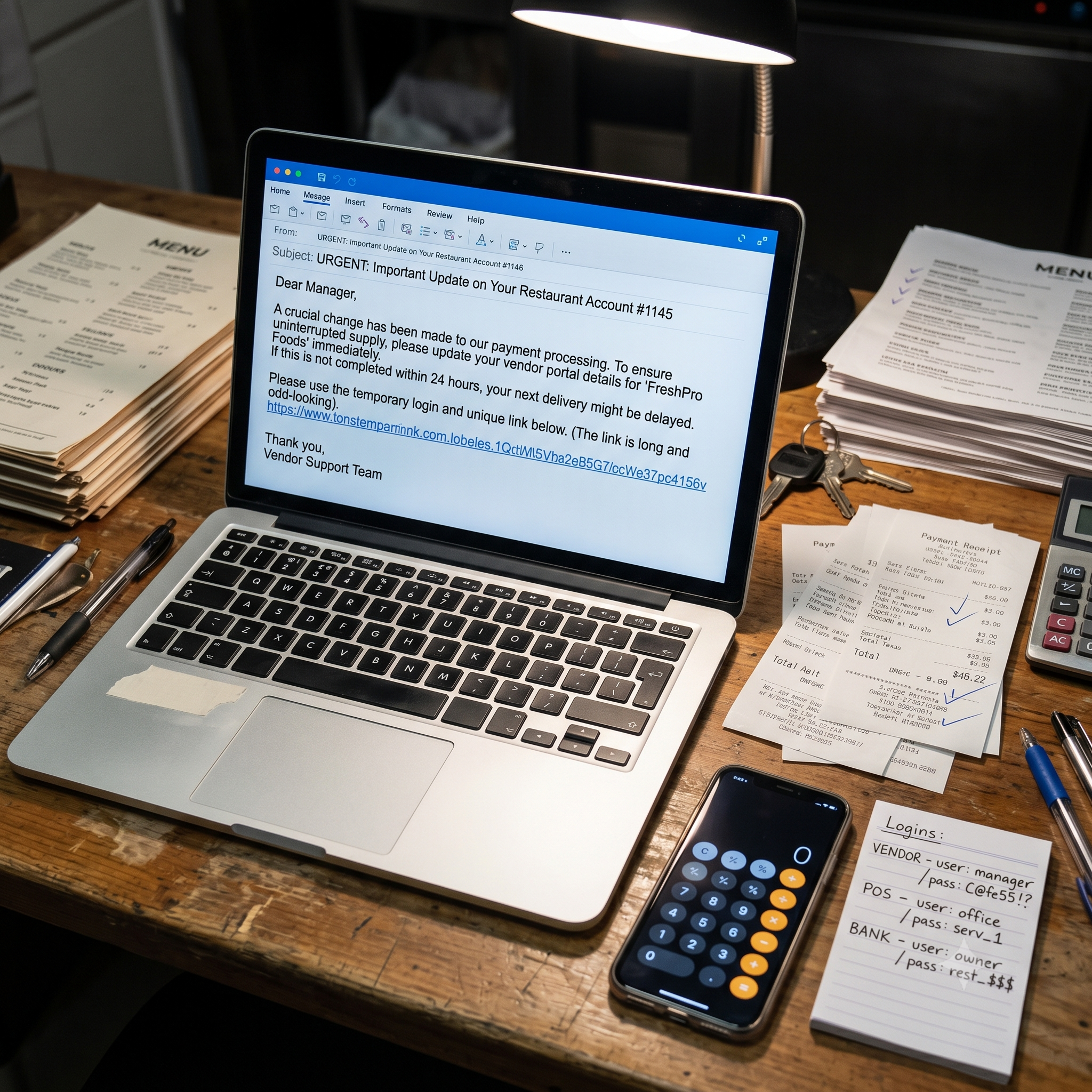

A cashier says one card took too long. A manager notices a login prompt that looks slightly unfamiliar. An email from a “service provider” asked for credentials earlier in the day, and now nobody is fully sure whether that message was legitimate. That sequence matters because restaurant payment cyber risk often grows out of routine business behavior. The FTC’s phishing guidance explains that scammers send messages that look ordinary and urgent, often trying to get people to click links, open attachments, or hand over passwords and codes. In May 2026, the FTC even highlighted a new phishing pattern using fake party invitations to capture email credentials. The method changes, but the structure stays the same: the message looks normal enough to get one rushed decision. (consumer.ftc.gov)

That is why this story works for restaurants. Restaurants are busy. Staff work under interruption. Managers split attention between vendors, payroll, reservations, guests, and service. That environment makes ordinary-looking digital requests more dangerous, not less. The FTC’s small-business guidance says companies should train employees, keep security current, and create systems for reporting suspicious activity because . scams often succeed when staff are distracted or rushed(ftc.gov)

In other words, restaurant payment cyber risk does not need a genius attacker to become expensive. It only needs one believable message, one weak password, one insecure remote connection, or one employee who thinks they are solving a quick business problem.

The Payment Screen Is Where Cyber Risk Becomes Visible

One reason owners underestimate cyber exposure is that much of it remains invisible until the money movement feels wrong. That is what makes the payment screen so important. It is the place where a restaurant’s digital systems, customer trust, and daily revenue all meet in public. The PCI Security Standards Council says small merchants should understand common payment systems and protect payment data because weak controls create openings for theft and fraud. Its merchant resources stress people, process, and technology, not technology alone. (pcisecuritystandards.org)

That is why restaurant payment cyber risk deserves its own focus instead of being buried inside generic cybersecurity advice. A breach or compromise tied to payments hits the most sensitive part of the customer relationship. The meal may be excellent. The service may be warm. But if the payment experience feels compromised, the business suddenly looks less stable than it did five minutes earlier.

In the story, the owner watches guests react in real time. Some wait patiently. Some become suspicious. One asks whether the terminal is safe. Another switches to cash. A third says they would rather leave than risk the issue. This is the operational side of restaurant payment cyber risk. The incident may begin in the background, but it becomes painfully visible at the point where a guest is asked to trust the business with money.

Restaurant Payment Cyber Risk Is Also a Reputation Story

The owner does not fear code. He fears what people will say.

That is realistic. Restaurants depend on repetition and trust. A customer does not just dine once. They come back and store loyalty details. Then, they use the same card again and recommend the place to friends. That is why restaurant payment cyber risk is not only about technical loss. It is also about reputational damage that can spread faster than the actual incident.

FTC guidance for small businesses says companies should protect customer information and prepare to respond quickly if systems are compromised because a data problem can hurt both operations and reputation. Its broader business-guidance pages treat cybersecurity as part of sound business conduct, not merely IT maintenance. (ftc.gov)

The story makes that easier to understand. The owner is not only wondering whether data was exposed. He is wondering whether his guests will trust the restaurant tomorrow. He is wondering whether one awkward payment afternoon becomes a permanent story customers tell. This is exactly why restaurant payment cyber risk belongs in restaurant management discussions, not just in technical vendor calls.

Weak Passwords and Remote Access Create Quiet Openings

In many small businesses, the most dangerous digital weaknesses are not dramatic. They are predictable. The PCI Security Standards Council says weak and default passwords are leading causes of payment-data breaches. It also warns that insecure remote access is another leading cause of breaches. Those two facts matter because they expose how mundane the starting point often is. (pcisecuritystandards.org)

That is a central reason restaurant payment cyber risk remains underrated. Restaurant owners often imagine that “real” cyber incidents require advanced tactics. But the official payment-security guidance points to much simpler openings: weak credentials, remote access mistakes, poor vendor control, and weak basics. The PCI small-merchant materials exist specifically because small operators may not have security teams, yet still hold valuable payment data and still face serious consequences if they lose control of it. (pcisecuritystandards.org)

In the story, the owner realizes that the problem was not high-tech sophistication. It was ordinary exposure left too ordinary for too long. That is a more unsettling lesson because it suggests the business was vulnerable in plain sight.

Restaurant Payment Cyber Risk Can Start With Vendor Trust

The owner trusted the vendor message because the message looked like part of the normal operating day.

That detail matters. Restaurants depend on outside systems and outside providers. POS support, payment processors, online ordering tools, inventory integrations, scheduling platforms, and email systems all create convenience. They also create trust pathways. FTC small-business guidance tells companies to assess cybersecurity risks posed by vendors and suppliers because third-party relationships can expand exposure. (ftc.gov)

This is one of the most useful ways to understand restaurant payment cyber risk. The threat does not always come from a random stranger pounding on the system. It often comes through a channel that already looks familiar. A fake invoice. A spoofed service request. A request to verify credentials. A message that arrives at the exact point where a busy manager is likely to act quickly instead of carefully.

The PCI Council’s merchant resources include “Questions to Ask Your Vendors” for a reason. Small businesses need a clearer way to evaluate who touches payment systems and how remote access is handled. (pcisecuritystandards.org) For restaurants, that is not a side issue. It is part of the payment workflow itself.

When Payment Problems Start, the Business Feels Exposed Fast

The story gets sharper once the owner realizes the problem is not going away in twenty minutes.

Staff start asking whether they should keep processing cards. Customers ask if they should worry. The owner tries to calm the room while also calling vendors, checking devices, and trying to understand whether any credentials were exposed. That is the point where restaurant payment cyber risk turns into a continuity issue. The restaurant may still be able to cook, but a restaurant that cannot collect payments confidently is not fully operational.

That is one reason PCI’s merchant guidance uses such direct language about protecting payment data and preventing breaches that can put a business out of operation. The Council is not describing a vague inconvenience. It is describing a direct threat to the merchant’s ability to function. (pcisecuritystandards.org)

The owner in the story sees that clearly now. The business did not lose its kitchen. It lost certainty at the register. In restaurant terms, that can be just as destabilizing in the short run.

Restaurant Payment Cyber Risk Is Harder Because the Business Must Stay Calm in Public

A restaurant cannot respond to disruption the same way a back-office business can.

Guests are physically present. Staff must keep moving. Payments happen in front of strangers. That is what makes restaurant payment cyber risk different from a quieter form of digital exposure. The problem enters the public room almost immediately. The owner cannot panic. The team cannot argue visibly about systems. Someone still has to explain what is happening without sounding confused or unsafe.

FTC guidance says businesses should prepare for scams and cyber incidents before they happen because the cost of confusion rises fast once the incident is active. (ftc.gov) The story shows that in human terms. A restaurant does not only need a technical response. It needs a guest-facing response, a staff response, and a business-continuity response all at once.

That is why restaurant payment cyber risk deserves more attention than it usually gets in hospitality media. It is not only technical. It is performative. The business must remain credible while its internal certainty is breaking.

The Business Learns That Cyber Risk Is Not Separate From Operations

By the end of the day, the owner understands the real lesson.

He thought cyber risk lived somewhere else. In the office or the cloud. Maybe in tech conversations. What he learns instead is that restaurant payment cyber risk sits directly inside daily service. It shapes the customer’s last impression and affects how staff work. In addition, it affects whether managers trust their own systems. This affects how fast the business can move without making the problem worse.

The National Restaurant Association’s Restaurant 2030 report is useful here because it says the restaurant industry’s future will be shaped by technology and data, not only food and service. That makes digital resilience part of restaurant resilience. (restaurant.org) Once that becomes clear, the payment screen stops being just a device. It becomes one of the restaurant’s most sensitive operational surfaces.

This is also where broader risk management becomes relevant. Restaurant owners often think about guest injuries, workers’ compensation, and property damage. They should. But the point of this story is that digital payment exposure now belongs in the same operational risk conversation.

What the Owner Wishes He Had Done Earlier

He wishes he had treated payment security like a routine management issue instead of a specialist issue.

That does not mean he needed to become a cybersecurity expert. It means he needed stronger basics earlier. The PCI Security Standards Council’s guidance for small merchants exists to make that possible. It focuses on foundational controls because most small businesses do not need theatrical cyber programs. They need disciplined basics: stronger passwords, safer payment handling, better vendor questions, better remote-access controls, and more staff awareness. (pcisecuritystandards.org)

FTC small-business guidance makes a similar point. The basics matter: train staff, keep software current, limit access, protect personal information, and prepare for scams before they happen. (ftc.gov) That is the practical lesson behind restaurant payment cyber risk. It is not mainly a story about elite technical defense. It is a story about whether the business respected the ordinary gateways through which digital damage often enters.

Why This Story Matters to Other Restaurants

The value of the story is that many restaurant owners will recognize themselves in it.

Maybe they have never had a real breach. Maybe they have only had weird card-reader behavior, strange emails, unfamiliar vendor prompts, or moments where the payment system felt a little too fragile. Those moments matter because they are often the early language of restaurant payment cyber risk. The actual breach or compromise may never come. Or it may come later, through the same weakness everyone already normalized.

That is why the story works as restaurant communication. It takes cyber risk out of the abstract and places it where owners already feel vulnerable: the daily transaction. This shows that the danger is not only data theft in theory. Then, it is lost confidence at the payment screen, confused staff, unsettled guests, and the creeping realization that the business depends on systems it has not questioned hard enough.

This is also where restaurant and entertainment insurance can fit naturally inside a broader preparedness conversation. The article is not saying insurance replaces security. It is saying restaurant digital exposure now belongs in the same serious business frame as other forms of interruption and liability.

A Practical Conclusion on Restaurant Payment Cyber Risk

“We never got robbed, but we still lost money like we had” is a useful way to understand the issue.

That line captures why restaurant payment cyber risk deserves more attention. The loss may not arrive through broken doors or visible theft. It may arrive through phishing, weak credentials, insecure remote access, vendor confusion, or a payment issue that suddenly makes the whole business feel less trustworthy. PCI’s merchant guidance says payment-data breaches can put a business out of operation. FTC business guidance says small businesses should train employees, protect systems, prepare for scams, and treat digital risk as part of protecting the bottom line. (pcisecuritystandards.org)

The sharp lesson is simple. In a restaurant, the payment screen is not the end of the guest experience. It is one of the places where the business can lose control fastest. That is exactly why restaurant owners should treat payment security as part of normal operations, not as an IT topic that lives somewhere else.