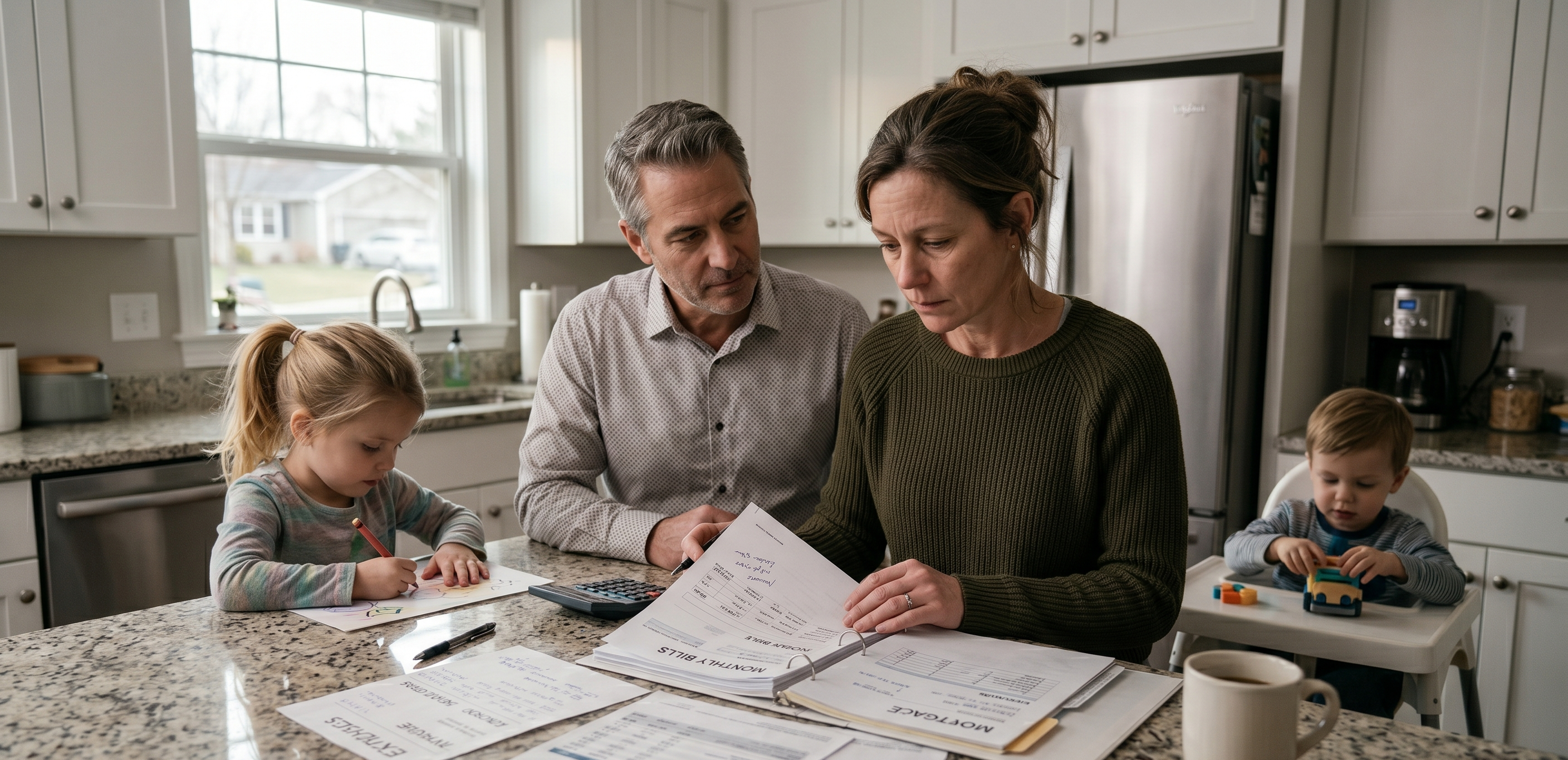

In many households, one paycheck still does most of the heavy lifting. That single income may cover rent or a mortgage, groceries, school expenses, transportation, insurance premiums, and the constant stream of monthly obligations that keep a family stable. That is exactly why life insurance for single-income families deserves more attention than it usually gets. That is why life insurance for single-income families is not a niche concern, but a practical financial protection issue.

Life insurance is often treated as something abstract, something to “get to later,” or something people assume will become important only when they are older or wealthier. In practice, the opposite is often true. For a family that depends heavily on one earner, the death of that person can create an immediate financial shock. The National Association of Insurance Commissioners explains that life insurance is designed to pay money to named beneficiaries when the insured dies, and its buyer’s guide notes that the death benefit can help address lost income, debt repayments, child care costs, and final expenses.

Why one income creates a bigger financial risk

The core purpose of life insurance for single-income families is to reduce the financial shock that follows the loss of a primary earner. The problem in a one-income household is not simply emotional loss, although that is obviously profound. The practical problem is concentration of risk. When one person provides most or all of the household income, the family’s economic structure becomes heavily dependent on that one life.

That dependence usually reaches further than people think. It is not just the salary itself. It is the mortgage qualification that depended on that salary, the car payment planned around that salary, the child care arrangement made possible by that salary, and the daily financial rhythm built on the assumption that the income will continue next month and the month after that.

The NAIC buyer’s guide frames the issue directly: people deciding how much life insurance they need should ask whether anyone depends on them financially, how much of the family income they provide, how final expenses and debts would be repaid, and whether existing employer coverage is enough to meet their obligations.

In a household with two strong, independent incomes, there may still be a serious disruption after a death, but the surviving adult may have some earnings base to rely on. In a household where one person’s income dominates, the margin for error is much smaller. The surviving family may need to make major decisions quickly, often while grieving: whether to move, whether to sell a vehicle, whether to pull children from certain schools or activities, whether to take on debt, or whether one parent must suddenly return to work under difficult conditions.

Life insurance is really about continuity, not just death

One reason people avoid this topic is that they associate life insurance only with mortality. But from a household planning perspective, life insurance is also about continuity. It is a way to create financial breathing room during a period when a family is least able to improvise.

The NAIC describes life insurance as a policy that pays a death benefit if the insured dies while the policy is in effect. That sounds simple, but the real meaning is broader. A life insurance benefit can help preserve housing, keep children’s routines stable, cover debts without forcing emergency decisions, and reduce the chance that grief is followed immediately by financial collapse.

That matters especially in households where the non-earning or lower-earning spouse is managing unpaid but essential work. A stay-at-home parent, for example, may not bring in wages, but that does not mean the family is less exposed. If the primary earner dies, the surviving spouse may face both income loss and a need to reorganize caregiving, employment, and household logistics all at once.

The hidden costs families forget to calculate

When families think about income replacement life insurance, many start with the obvious monthly bills. That is reasonable, but it is often incomplete. The direct paycheck is only one part of the risk.

The NAIC buyer’s guide specifically mentions financial hardships such as loss of income, funeral expenses, medical or nursing care expenses, debt repayments, and child care costs. It also highlights continued needs like family support, children’s education, and paying off a mortgage.

In practice, the overlooked costs may include:

- temporary child care or after-school supervision

- transportation changes if one adult must start commuting differently

- legal or estate administration expenses

- relocation costs if housing becomes unaffordable

- therapy or counseling support for children and surviving adults

- the loss of employer-linked benefits tied to the deceased person’s job

Even when a family receives some public support, it may not come close to replacing what was lost.

Why Social Security survivor benefits are not the same as life insurance

Many households assume that if the primary earner dies, Social Security will broadly take care of the family. That assumption can lead to underinsurance.

The Social Security Administration states that survivor benefits provide monthly payments to eligible family members of people who worked and paid Social Security taxes before they died. Eligibility may include a spouse, divorced spouse, child, or dependent parent, and the SSA notes that benefits can provide a monthly payment and, in some cases, Medicare eligibility based on the deceased worker’s record.

That support matters. But it is not the same as full income replacement. It may not match the deceased earner’s paycheck, it may not cover all dependents in the way the family expects, and it does not automatically solve mortgage debt, education plans, or the broader financial restructuring that often follows a death. Social Security survivor benefits are part of the safety net, not a substitute for deliberate household planning.

This is one of the most important misunderstandings in single-income households. Families often discover too late that “some support” is very different from “enough support.” For that reason, life insurance for single-income families should not be confused with public survivor support.

Why life insurance for single-income families is often most urgent in ordinary middle years

A common mistake is assuming life insurance matters most only for the wealthy or elderly. In reality, the financial vulnerability is often greatest during ordinary middle years, when families are carrying heavy responsibilities but have not yet built major assets.

That stage often includes a mortgage, children still at home, debt balances, limited savings, and an entire family budget structured around one primary earner. These are precisely the years when term life insurance is often discussed because, as the NAIC explains, term life insurance is designed to provide lower-cost coverage for a specific period. It pays the named beneficiaries if the insured dies during that term.

For many families, that period of highest vulnerability may be 10, 20, or 30 years: the years needed to raise children, pay down a home loan, or build enough savings that the household would no longer collapse if one paycheck disappeared. This is why the conversation is not mainly about age. It is about dependency.

The question is not “Do we need it?” but “What would happen without it?”

Families sometimes approach this decision the wrong way. They ask whether life insurance feels necessary right now. A better question is more concrete: what would actually happen to the people who depend on this income if it stopped permanently next month?

Would the mortgage still be payable? Could the surviving spouse stay home with young children, or would immediate employment become necessary? Would debts need to be settled by selling assets? Would older children have to take on financial responsibilities early?

The NAIC’s coverage guidance is essentially built around these questions. It recommends thinking through who depends on you financially, how much income you provide, and how the family would handle debts and final expenses after your death.

That framework is useful because it shifts the discussion away from vague fear and toward practical planning. A household does not need to predict every future expense perfectly. It simply needs to take the dependency seriously.

Term coverage is often the starting point for family income protection

For families focused primarily on protecting dependents during the years of highest vulnerability, term coverage is often the most straightforward entry point.

The NAIC says term life insurance is purchased for a period of time and is intended to provide lower-cost coverage for a specific period. It can also sometimes be renewed, though premiums may rise significantly later, which is why policyholders should ask how renewal terms work and whether the right to renew ends at a certain age.

That matters for one-income families because affordability is part of the decision, not a side issue. A policy that looks appealing on paper but becomes hard to maintain under real household conditions may not solve the problem. The NAIC buyer’s guide also stresses that people should be sure they can afford the premium and ask whether higher future premiums would still be manageable.

This is where many practical households land: they are not necessarily looking for a complicated product. They are looking for a reasonable way to create financial protection during the years when one income supports multiple lives.

Employer coverage may help, but it may not be enough

Another common assumption is that employer-provided life insurance solves the issue. Sometimes it helps, but relying on it alone can be risky.

The NAIC buyer’s guide notes that while people may have free or low-cost life insurance through an employer, the death benefit is usually less than they need, and if they leave the employer they may not be able to take that coverage with them.

That has two important consequences. First, a family that depends on one paycheck may be much more exposed than it realizes if it has never compared employer coverage with real household obligations. Second, job changes can quietly remove part of the family’s safety net at exactly the wrong time.

For households already managing a tight budget, this issue is easy to miss. A family may feel “insured” because a benefit exists at work, but that is not the same as confirming that the amount and portability of that benefit actually match the household’s risk.

Beneficiary decisions matter more than people think

Life insurance planning does not end with buying the policy. Beneficiary choices can shape how smoothly benefits are received and whether the intended people can actually access the funds.

The NAIC explains that life insurance pays money to named beneficiaries, and its beneficiary guidance stresses the importance of informing beneficiaries or trusted advisors that a policy exists and keeping policy information in a safe place. The same guidance notes that the NAIC Life Insurance Policy Locator can help find unclaimed benefits when families do not know where a policy is or whether one exists.

This point is often underestimated. A family can do the hard part of buying coverage and still create problems later if the beneficiary designations are outdated, unclear, or never discussed. In single-income households, that is especially important because the surviving dependents may be relying on those funds quickly.

The broader lesson is simple: protection is not only about having a policy. It is also about making sure the benefit can reach the right people without unnecessary confusion.

Affordability should be judged against household fragility

People sometimes reject life insurance because they do not want another monthly bill. That concern is understandable, especially for families already operating close to the edge. But the affordability question should be framed correctly.

The relevant comparison is not only “Can we fit this premium into the budget?” It is also “How financially fragile is this household without any protection?” For a one-income family, the absence of coverage may mean that one death could trigger housing insecurity, debt distress, or forced lifestyle collapse.

The NAIC’s buyer’s guide emphasizes affordability and warns consumers to understand whether premiums could rise and whether they could still keep coverage in force. It also notes that policies requiring less health information may cost more and provide less coverage than policies with fuller underwriting.

In other words, affordability matters, but so does timing. Waiting too long can narrow options or change pricing. A family that knows it is heavily dependent on one income is not just shopping for a product. It is managing concentrated financial risk.

A single-income household is also a dependency network

One useful way to think about this issue is to stop picturing a one-income family as simply “one worker and several dependents.” In reality, it is a dependency network. The earner supports not only household consumption but also stability, planning, time allocation, and future options.

Children depend on that network. A spouse may depend on it while handling unpaid caregiving work. Elderly relatives may be indirectly connected to it. Long-term plans such as college savings, homeownership, or relocation may all rest on one stream of income continuing.

That is why the decision around life insurance for one-income households is not merely about replacing a salary number. It is about preserving a structure. Once that becomes clear, the logic of coverage becomes easier to understand.

Why this discussion matters for business owners too

This issue is not limited to salaried employees. For small business owners, contractors, and self-employed households, the dependency can be even more severe. A family may depend not only on the owner’s labor, but also on the owner’s relationships, decision-making, and ability to keep revenue moving.

That makes the loss of the primary earner potentially more disruptive, not less. In some cases, family and business risk are tightly linked. A household depending on one business owner may need to think not only about family expenses, but also about outstanding obligations, continuity planning, and broader risk management around the owner’s death. CIS, for example, positions itself around commercial insurance and risk management across multiple states, while also offering life insurance solutions relevant to families and business owners thinking about protection in a broader financial context.

That does not change the core household principle. It reinforces it. When one person carries the economic structure, the cost of inaction is often hidden until the worst moment.

The calm conclusion many families need

The life insurance conversation is often delayed because it feels uncomfortable, complicated, or emotionally heavy. But in single-income households, delay can be its own financial decision.

The practical case for coverage is not dramatic. It is simple. When one person’s income supports the family, the household has a concentrated vulnerability. Life insurance exists to reduce the damage that vulnerability can cause. The NAIC’s consumer guidance makes clear that life insurance is meant to protect against hardships such as lost income, debt, child care costs, and final expenses, while Social Security confirms that survivor benefits may help but are limited to eligible family members and defined payments based on the deceased worker’s record.

For families, the most useful question is not whether the topic is pleasant. It is whether the people who depend on one income would be financially protected if that income disappeared. In many households, that answer is still no. In the end, life insurance for single-income families is about preserving stability when one income supports several lives.